I hate to be a wet blanket, but the American consumer isn’t coming back and the consequences of this fact have yet to be realized by the financial markets, foreign manufacturers, domestic retailers or politicians. The overhang of debt, continued home price depreciation, lack of savings, and aging of America will change the face of retailing for decades.

Why Worry?

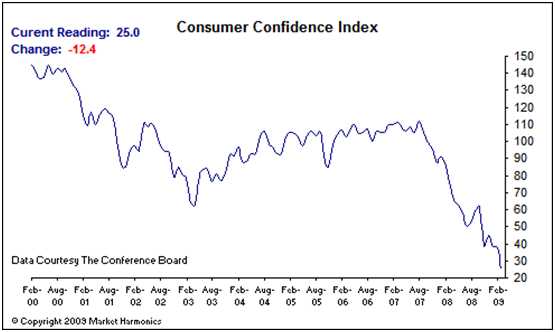

The Consumer Confidence Index in February was 25, the lowest since the index inception in 1967. During the Dot.com bubble it reached an irrationally exuberant 140. It hovered in the 110 level through the housing bubble until late 2007. The good news is that it can’t go below zero. The CNBC pundits and Washington politicians think that Americans just need to get their confidence back and everything will be OK. There’s only one problem. You can’t spend confidence.

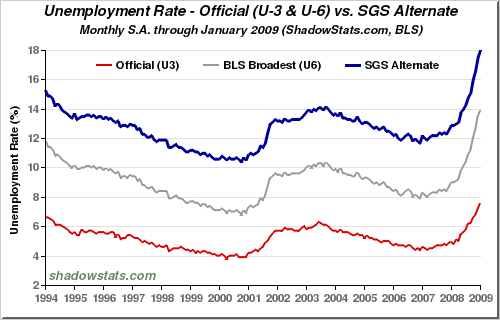

The index shows how fragile the psyches of Americans can be. In retrospect, the extreme confidence in early 2000 and high levels from 2004 through 2007 were completely unwarranted. The American public had a false sense of confidence inflated by our bubble economy. Now the confidence level is at a record low level. This level is rational. With the government reported unemployment rate of 7.6% and the true rate between 14% and 18%, consumers aren’t too confident. There are 235 million Americans of working age. Only 154 million are in the work force according to government statistics. Of those, 11.6 million are unemployed. There are 81 million Americans of working age who are not in the workforce. At least 10 million of these people would work if they had an opportunity. With the massive destruction of wealth in the last two years, many more of the 81 million will have to go back into the workforce, whether they like it or not.

The Long and Unwinding Road

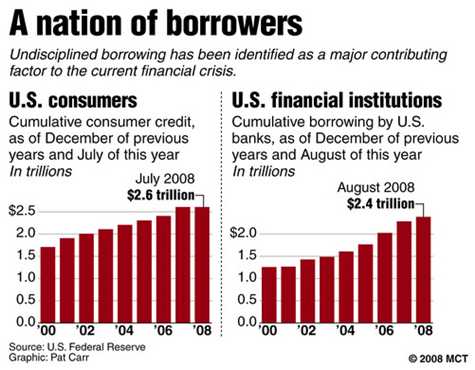

The country has tried to spend its way to prosperity over the last three decades. Total consumer debt is just under $2.6 trillion, or $23,600 per household. This includes credit card debt, auto loans, and personal loans. There are approximately 170 million credit card holders who own 1.5 billion cards, or 9 cards per person. The average household carries nearly $8,700 in credit card debt. The average new car loan is $25,000 with a loan to value ratio of 93%. This means that the average new car owner is underwater on their loan as soon as they pull out of the dealership parking lot.

The credit card wasn’t invented until 1967. Americans have adapted quite well to this newfangled American invention. Since 1970 revolving credit debt has increased by 26,000%, from $3.7 billion to $963.5 billion. Over this same time frame GDP grew by 1,430%. These statistics prove to me that America has maintained its standard of living by using credit cards. The always loquacious Alan Greenspan concluded in 2005 that the geniuses at Citicorp (C), Bank of America (BAC), and Capital One (COF), among others, had done a wonderful service to humanity by giving credit cards to people who could not pay them back. I can picture his hang dog jowls quivering while tears welled up in his lying eyes.

As we reflect on the evolution of consumer credit in the United States, we must conclude that innovation and structural change in the financial services industry have been critical in providing expanded access to credit for the vast majority of consumers, including those of limited means. Without these forces, it would have been impossible for lower-income consumers to have the degree of access to credit markets that they now have. This fact underscores the importance of our roles as policymakers, researchers, bankers, and consumer advocates in fostering constructive innovation that is both responsive to market demand and beneficial to consumers.

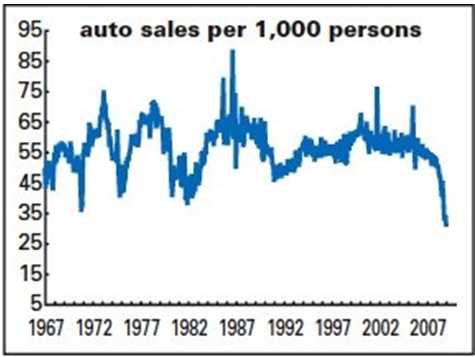

Only 23% of the credit cards in the country are in the hands of prime borrowers. Giving out credit cards like candy to people of limited means couldn’t possibly end badly. The MBA Wall Street geniuses gazed at their models and concluded that their million dollar bonuses were in the bag. According to Fitch, write-offs are breaching 8% and are headed towards 10%. Auto loan delinquencies are already at 10%. Maybe lending 120% of the value of those Cadillac Escalades to a person with no job or assets was a bad idea.

The worst recession since the Great Depression will lead to the unprecedented credit card write-offs. Guess who will step up to the plate and cover these losses? Right again. You and I will pay for the noble experiment of giving credit cards to people with little or no income. The bank CEOs walked away with hundreds of millions in pay, Congressmen who pushed for poor people to get the credit were re-elected, Alan Greenspan receives $150,000 per speaking engagement, and the U.S. taxpayer gets screwed.

Next Page 1 | 2 | 3 | 4 | 5 | 6 | 7

(Note: You can view every article as one long page if you sign up as an Advocate Member, or higher).