Today the financial media was abuzz about a Justice Department suit against Standard & Poor's. So I thought it might be worthwhile to repost this roadmap to a Justice Department lawsuit, first presented on August 30, 2011.

Dear Justice Department,

So far, major investigations by the S.E.C., by the Financial Crisis Inquiry Commission, and by the Senate Subcommittee on Permanent Investigations have let the rating agencies off the hook. They found that the agencies were far less diligent and conscientious than they should have been, and were therefore slow to appreciate the implications of the real estate bubble and slow to take corrective action. In other words, they failed to do their job but they weren't crooked.

Top rating agency executives, who have no shame, disagreed. Moody's CEO Ray McDaniel, whose travesty of corporate governance helped cause damage 100 times worse than that caused by Enron or the Madoff Fund, refused to accept any real blame. Neither he nor his top deputies have been held to account for their malfeasance and their cover-up.

Now, your new investigation presents a chance to pick up where the others left off. This letter offers a roadmap for jumpstarting the process. One pitfall you want to avoid is getting bogged down with the incessant dissembling from rating agency executives. If you listen to the FCIC interviews of the top people at Moody's, you'll notice that they talk forever but refuse to be pinned down on anything. They are very clever and adept at muddying the waters. But as we'll see, it is very easy to prove that virtually every single subprime and Alt-A mortgage securitization, and every single CDO comprised of mortgage securities, was rated under false pretenses.

Numbers Frame The Narrative

To proceed, you need to think like Harry Markopoulos, who, upon reviewing the preposterous financial results of the Madoff Fund, said, "I knew he was a fraudster in five minutes." Remember, in finance and business the narrative is always framed by the numbers, not by what people say. And if you start with the numbers and work backwards, it quickly becomes apparent how people were lying and deceiving.

Markopolos did have that rarest of rare qualities, a willingness to say that the emperor has no clothes. Over the past decade, few have been willing to declare that the emperors who defined reality in mortgage finance had no clothes. And from what I've been told, many who wanted to speak out were fearful of retribution or blacklisting.

Thankfully, the numbers on mortgage securities, reduced to their bare essentials, are easy to understand. You don't need an advanced background in statistics to prove that the ratings processes had devolved into a complete sham. If you let the numbers frame your inquiry, you won't find a single smoking gun; you'll find thousands of smoking guns.

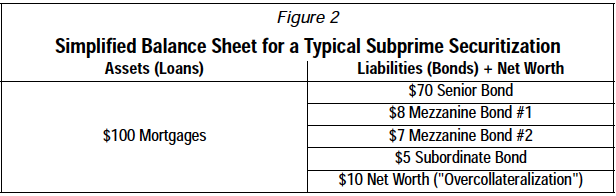

Here's simple but emblematic example, a deception that was repeated by Moody's executives Warren Kornfeld, Michael Kanef and Jay Siegel. When people started getting nervous about the sector, they presented the "Typical Subprime Securitization," which was structured with 10% equity, or overcollateralization.

Such a thing never existed. There never was any "Typical Subprime Securitization" structured to close with 10% overcollateralization, just as there was never any "typical ballerina," who weighed 300 pounds, or any "typical McDonalds hamburger," priced at $50. The initial equity tranche or overcollateralization on any subprime deal was invariably between 3% or 4%. These Moody's executives wanted to promote the false impression that the structures and ratings were devised with some reasonable margin for error, which was definitely not the case. The deals were structured with virtually no margin for error, because they relied on garbage-in/garbage-out ratings methodologies.

Their example also showed that if a mortgage pool incurred a 20% loss, the "senior bond" would not be impaired. In fact, a 20% loss meant that all of the principal on tranches rated double-A, single-A and triple-B got wiped out. When Kormfeld first presented this example on April 19, 2007, a total writeoff on a double-A-rated bond seemed unimaginable. And by April 19, 2007, it was clear as day that every single subprime mortgage bond issued during the past two years would suffer big losses on its investment grade tranches.

This "typical subprime securitization" falsehood touches on two of The Three Big Myths, which are rating agency mantras. They are:

1. We rated these mortgage securities in good faith;

Next Page 1 | 2 | 3 | 4 | 5 | 6 | 7

(Note: You can view every article as one long page if you sign up as an Advocate Member, or higher).