The organization lacks independence from the insurance industry. Skepticism about the organizations effectiveness is well justified.

NAIC is governed by twelve elected and thirty-eight appointed state health commissioners. Those running for election need campaign funds. Insurance companies are major contributors. Those appointed gain the office from governors. For the appointed, the contributions are just one-step away from the commissioners.

Elected and appointed commissioners have hefty political baggage. These are not the type of objective analysts and thinkers you want writing critical regulations that will affect your health.

These are just some of the reasons to expect little or no change in rates for those who purchase their insurance directly, primarily the self employed and small business owners. Were there any reason to expect change, the change should have arrived by now.

On October 21, 2010, we saw the future. NAIC announced that it had completed its model regulations on medical loss ratios. On the very same day, Kathleen Sebelius, Secretary of Health and Human Services (HHS), announced that:

"We will work quickly to promulgate this regulation, using the NAIC recommendations as a basis, because we believe these new policies will help ensure not only cost savings but higher quality care for consumers. We look forward to working closely with NAIC throughout the process." Kathleen Sebelius, Secretary HHS, October 21, 2010

Sebelius must be a very fast reader. I hope that she will read about the total failure of her favorite regulatory authors to gain any "cost savings' while they regulated insurance rates in their states for the self employed and small business. Then she might realize that "care for consumers" is not possible without affordable health care.

Don't hold your breath.

END

This article may be reproduced entirely or in part with attribution of authorship and a link to this article.

Appendix

I. Tax breaks to very small business

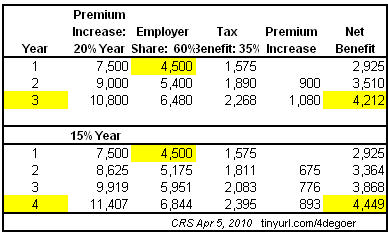

The tax provisions of the health care act were supposed to help very small businesses afford insurance for their employees. It appears that the tax breaks will lose their utility about the time that they expire. While they offer initial savings, premium increases wipe out the benefits of the tax cut in year three using the 20% per year increase and year four using the 15% premium increase.

From: Summary of Small Business Health Insurance Tax Credit Under PPACA (P.L. 111-148) Congressional Research Service, April 5, 2010

II. The Influence of National Association of Insurance Commissioners (NAIC)

(Note: You can view every article as one long page if you sign up as an Advocate Member, or higher).